Individuals 50 of 6,140 results

Organisations 50 of 8,158 results

Buzzes 50 of 12,424 results

LGIM: Active Ownership Report 2023

LGIM: Active Ownership Report 2023

(https://www.lgim.com/uk/en/responsible-investing/active-ownership/)

'Our Active Ownership report details how our Investment Stewardship and Investment teams exercised voting rights across our entire book and engaged with companies, policymakers and other stakeholders with an aim to deliver positive change on topics including deforestation, income inequality, human rights and artificial intelligence.'

William Blair: Metals of the Future: Set to See Continued Growth (Blogpost)

William Blair: Metals of the Future: Set to See Continued Growth (Blogpost)

(https://www.williamblair.com/Insights/Metals-of-the-Future-Set-to-See-Continued-Growth)

Metals like copper, lithium, and nickel entered the spotlight recently as high demand from new economic sectors has been transforming their markets. Propelled partly by the green energy revolution, we have seen increased investments and innovation in these metals to meet the growing demand for renewable energy.

Alexandra Symeonidi, CFA, is a corporate credit analyst on William Blair Investment Management’s Emerging Markets Debt team. Covering the oil and gas, metals and mining, industrials, and utilities sectors across emerging markets, Symeonidi's recent work explores the reasons behind the metals’ growth and demand.

Allianz GI: Sustainability and Stewardship Report 2023

Allianz GI: Sustainability and Stewardship Report 2023

The report highlights 2023 key developments:

AllianzGI further built out its sustainable investing offering. There are now more than 200 sustainable funds that are classified as Article 8 or 9 according to the European Union (EU) SFDR regulation , accounting for 61% of AllianzGI’s total mutual fund AuM.

Capitalising on the successful Key Performance Indicator (KPI) approach targeting decarbonisation, AllianzGI introduced two new sustainable investment approaches in 2023:

a) the ESG score approach that targets a higher weighted average ESG score in comparison to the benchmark and is applied to emerging market strategies

b) a KPI sustainable investment share approach that directly leverages AllianzGI’s proprietary methodology to identify sustainable investments, according to the SFDR.

Successful introduction of new and innovative fund solutions. Examples are the launch of the company’s first social-focused equity strategy and the closing of the SDG Loan Fund, a “blended finance” strategy established together with MacArthur Foundation and FMO IM that mobilised USD 1.1 billion in investor capital to advance the United Nations Sustainable Development Goals (SDGs) in emerging and frontier markets.

Intentions for 2024

AllianzGI’s Sustainability and Stewardship Report also looks ahead and outlines aspirations for 2024.

In the current year, the political agenda risks delaying the financing and implementation of transition plans. This can result in a higher probability of a “delayed transition” scenario. AllianzGI is already providing advisory analysis on the potential impact on client portfolios in terms of the drag on returns under different climate scenarios reflecting increased systemic risk.

Moreover, 2024 could be the year when biodiversity – a topic that typically attracts less attention than climate change as an environmental concern – gets the attention it deserves. The integration of biodiversity into the investment process will likely be accelerated, and AllianzGI expects this to stimulate further client interest and new product development.

Allianz GI: Avoided emissions: how investors can judge companies’ net-zero credentials

Allianz GI: Avoided emissions: how investors can judge companies’ net-zero credentials

Allianz GI: Avoided emissions: how investors can judge companies’ net-zero credentials

The increasing frequency and severity of weather-related events due to climate change has highlighted the urgent need to take action and achieve net-zero greenhouse gas (GHG) emissions by 2050.1 Investors can turn to “avoided emissions” – the positive impact of a more sustainable product or service – to assess which potential investments can make the most significant contribution to achieving this target.

Key takeaways

- Avoided emissions reflect emissions savings achieved by a product, service, or project in wider society. Avoided emissions is a key complementary metric to more established scope 1, 2 and 3 measures.

- Climate solutions such as solar, wind, grid technologies and sustainable biogas are key to boosting avoided emissions.

- There is a lack of methodological clarity around avoided emissions, but greater application across private and public markets will formalise measurement approaches.

- Measures of avoided emissions can help channel investment to solutions that make the most significant contribution to achieving net zero emissions by 2050.

VBDO: Biodiversity and Business - Challenges and good practices

VBDO: Biodiversity and Business - Challenges and good practices

VBDO: Biodiversity and Business - Challenges and good practices

The past five decades have seen a rapid deterioration in our global ecosystems. Research by the UN Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), shows that biodiversity is under enormous pressure from human activities. The WWF Living Planet Report describes that one million species – out of an estimated eight million in total – are threatened with extinction.

Most companies have taken action to reduce their impact on biodiversity, but at the same time are struggling to find the right approach, the report notes. From the interviews conducted, this is mostly due to the complexity of the subject: there are many different factors involved in effectively reducing negative impacts on biodiversity. For instance, the focus is usually on climate change, while four other causes need at least as much attention, such as countering pollution and the spread of invasive plant and animal species.

Good practice instead of best practice

The report stresses that it is crucial for companies to be aware of their impacts and to understand the dependencies within their business models. In this way, they can make changes appropriate to their operations and the areas in which they operate

Nordea Asset Management: Semiconductors – the brain of energy efficiency

Nordea Asset Management: Semiconductors – the brain of energy efficiency

(https://www.nordeaassetmanagement.com/insights/semiconductors-the-brain-of-energy-efficiency/)

Looking back two years, can you still remember the shortage of numerous products towards the end of the pandemic? Consumers were facing shortfalls of products ranging from televisions and cellphones to cars, WiFi routers, medical devices and gaming consoles, among many other things. A central reason was a global shortage of semiconductors, also known as microchips and integrated circuits, mainly due to the effects of the Corona crisis causing disruptions in the supply chain.

The shortage of semiconductors had a serious impact on industrial companies worldwide. The automotive industry was hit hardest: production lines been stopped, employees were put on short-time work, new cars had an analogue speedometer instead of a digital version or had to do without certain assistance systems. But a lack of microprocessors didn’t hit only the automotive industry hard. Goldman Sachs identified 169 industries that suffered from the ongoing chip shortage.

Digitalization and therefore microelectronics are moving into all areas of life. With their diverse areas of application, semiconductors play a central role in the materials of electronics and energy technology.

Semiconductor chips are incredibly complex. State-of-the-art devices can contain over one billion circuit elements. There is simply no way to manage this level of complexity without sophisticated automation. Electronic Design Automation (EDA) provides this critical technology.

In this industry with high relevance to the global economy, US company Cadence Design Systems is one of the largest provider of EDA technology with a market share of 30% while dominating the analog design part of the market with around 70% share.

Nordea Asset Management: Waste – an opportunity not to be wasted

Nordea Asset Management: Waste – an opportunity not to be wasted

(https://www.nordeaassetmanagement.com/insights/waste-an-opportunity-not-to-be-wasted/)

The world is drowning in garbage. At least that’s the impression you might get if you look at the forecasts for the projected global increase in waste: For 2050, the World Bank predicts a growth in the annual global waste generation from the current around 2 billion to 3.4 billion tons – an increase of around 70%. This represents more than double the population growth over the same period.

Worldwide, only 14% of waste gets a “second life”. Much of what cannot be recycled is burned to generate energy. The problem is that this increases global carbon dioxide emissions and is therefore harmful to both humans and the climate.

GFL Environmental – Waste is their business

GFL Environmental is one of the top 5 waste management companies in North America. With a compound annual revenue growth rate of 32% over the past five years, GFL has become the fastest-growing U.S.-listed municipal waste management company.

HSBC: Climate investment update - Rethinking the ESG narrative: the case of the EU Green Deal

HSBC: Climate investment update - Rethinking the ESG narrative: the case of the EU Green Deal

- The EU Green Deal is alive and well, but successful implementation requires an integrated economic narrative

- Fierce global competition in many clean and transition techs reveals uncomfortable lessons for EU green industrial policy

- In our view, getting policy right could reduce the cost of capital while increasing investment returns and growth

Clients of HSBC Global Research can access the full report via the HSBC Global Research website or by contacting Wai-Shin Chan

Contrary to popular opinion, the Green Deal is alive and well. Despite some watering down and political surprises - to be expected ahead of elections - it continues to provide a strong foundation to achieve Europe's 2030 climate targets.

However, we think a shift in narrative and mindset is needed to implement it successfully post June's EU Parliamentary elections. Examining climate policy in a silo and imposing this on the economy will no longer work. Green Deal implementation needs to start with consideration of socio-economic factors first, including rapidly shifting geopolitics, changing trade flows, monetary and fiscal policy, changing industrial competitiveness, and so on, and then fully integrate green.

In our view, this approach could reduce the risks of pushback and a stop-start transition, which would be detrimental to corporate value and investment returns.

Planet Tracker: Leaders and Laggards in Chemical Industry's Transition to Net Zero Emissions

Planet Tracker: Leaders and Laggards in Chemical Industry's Transition to Net Zero Emissions

(https://planet-tracker.org/wp-content/uploads/2024/04/Tomorrows-Chemistry.pdf)

Planet Tracker: Leaders and Laggards in Chemical Industry's Transition to Net Zero Emissions

The chemical industry, generating USD 5.7 trillion in annual revenues (2022) and directly employing over 15 million people, plays a pivotal role in the global economy.

Its products are integral to various sectors, making chemical components essential for 96% of all manufactured goods.

The journey towards sustainability in this sector, especially in producing key chemicals like ammonia, methanol and ethylene, is critical for the broader transition to a global Net Zero economy.

Planet Tracker’s report, Tomorrow’s Chemistry, presents a comparative analysis of the Climate Transition Assessments (CTAs) of seven leading chemical companies, Air Liquide, BASF, Bayer, Dow, Incitec Pivot, LyondellBasell and Toray Industries.

After assessing their commitments, strategies and readiness to align with the Paris Agreement and achieve Net Zero emissions by 2050, Planet Tracker's ranking identifies Air Liquide as the clear leader in the analysis, while BASF sits at the bottom of the ranking.

View the Best Practice Guideline

Download the Investor Engagement Sheet

AXA IM: Hold steady: Sustainability in the face of polycrisis (podcast)

AXA IM: Hold steady: Sustainability in the face of polycrisis (podcast)

In the face of the global polycrisis of war, climate change, slow growth, and political instability, corporate leaders are revaluating their net zero commitments to prioritize concerns such as supply chain resources, high interest rates, and declining consumer demand amid a cost-of-living crisis.

In this episode of Sound Progress, our host Herschel Pant speaks to:

- Simon Rawson, Deputy Chief Executive of ShareAction

- Gilles Guibout, Head of European Equity Strategies at AXA IM; and

- Héloïse Courault, Senior Corporate Governance and Stewardship Analyst at AXA IM

... about shifting corporate priorities and why it is important that CEOs to hold steady on their sustainability commitments.

Robeco: SI Dilemma: How important is the G in ESG?

Robeco: SI Dilemma: How important is the G in ESG?

(https://www.robeco.com/en-int/insights/2024/04/si-dilemma-how-important-is-the-g-in-esg)

Robeco: SI Dilemma: How important is the G in ESG?

We have discussed the competition and interaction between E and S in this column before, but not the G in ESG.

In fact, looking at the range of sustainable investment strategies in the market, it would be fair to think that the G is often neglected!

Summary

- Governance can seem neglected compared with the E and S

- Agreement on financial materiality, but impact materiality requires judgement

- The G is actually everywhere – a necessary foundation for SI strategies

HSBC: ESG and Data Science - Unraveling corporate mentions and meaning of ESG

HSBC: ESG and Data Science - Unraveling corporate mentions and meaning of ESG

- What are companies saying about ESG? We apply our bespoke natural language processing model to corporate earnings calls

- Mentions of the term "ESG" have fallen to almost zero in the US amid pushback; Europe and LatAm still use the term...

- ...but whether they say the word "ESG" or not, companies continue to comment on related themes

Clients of HSBC Global Research can access the full report via the HSBC Global Research website or by contacting Wai-Shin Chan

|

Klement on Investing: Reshoring leads to more global trade

Klement on Investing: Reshoring leads to more global trade

PGIM: Great expectations - Is engagement living up to its promise?

PGIM: Great expectations - Is engagement living up to its promise?

(https://cdn.pficdn.com/cms1/pgim4/sites/default/files/PGIM-ESG-Great-Expectations-0424.pdf)

Is ‘engagement washing’ poised to be the next term maligning asset management’s ESG movement?

Institutional investors often engage with companies they invest in to improve those companies’ environmental, social and governance practices— rivalling capital allocation as a core mechanism for achieving sustainable investment outcomes. But do engagement activities really deliver impactful, positive, real-world outcomes?

As a growing number of institutional investors make ambitious sustainability commitments, the volume of engagement activity reports grows with them. Company interactions on sustainability topics are commonplace, the range of engagement themes has widened, and goals have become loftier. Meanwhile codes of best practices are evolving to encourage a focus on real-world outcomes in engagement reporting, in contrast to the investment outcome focus of just a few years ago.

Yet, there is a growing realisation – and genuine bewilderment – that engagement for positive sustainability outcomes is not living up to the expectations of its proponents. When it comes to mitigating the negative impacts of certain economic activities on our environment and society, engagement can be influential, but it is rarely transformational—and an engagement expectation gap is emerging.

Zevin Asset Management: Unleashing Impact Through Gender Lens Investing

Zevin Asset Management: Unleashing Impact Through Gender Lens Investing

Gender lens investing offers investors a process for identifying and weighing issues pertaining to gender-based issues — pay equity, gender diversity, and career advancement, to name a few. Zevin AM integrate these findings into their investment decision-making with the goal of mitigating risk, identifying opportunities, and creating positive social impact.

Only about 12.5% of portfolio managers across U.S.-based funds in 2022 were women, almost unchanged from the previous ten years, according to Morningstar. The financial services industry has historically been unwelcoming to women given toxic working environments stemming from a culture of bullying, misogyny, and sexual harassment. Changing that culture is one aspect of Zevin's approach to gender lens investing.

Gender lens investing includes supporting shareholder proposals that seek to expand disclosure of workforce diversity or to improve or adopt policies that promote an inclusive workplace. Zevin AM believe shareholder requests for improving workforce diver sity, equity and inclusion (DEI) position a company for long-term success.

Impak Analytics: SFDR: Wait or anticipate?

Impak Analytics: SFDR: Wait or anticipate?

(https://www.impakanalytics.com/sfdr-wait-or-anticipate/)

Impak Analytics: SFDR: Wait or anticipate?

Our case study provides the keys to a clear, rigorous methodology for analyzing positive contributions through the concrete problems of an asset manager and two renowned companies such as L’Oréal and Vestas.

It is a real guide for FMPs who want to avoid the pitfalls of greenwashing and thus comply efficiently with the SFDR while preparing its next version.

WHEB: FP Sustainability Fund - Q1 2024 Report and Datapack

WHEB: FP Sustainability Fund - Q1 2024 Report and Datapack

The quarterly review for Q1 2024 for the WHEB Sustainability Fund.

WHEB: Stewardship in the Spotlight: Managing micro-pollution

WHEB: Stewardship in the Spotlight: Managing micro-pollution

(https://www.whebgroup.com/our-thoughts/stewardship-in-the-spotlight-managing-micropollution)

Micro-pollutants: Unseen yet ubiquitous It’s an unfortunate reality that by the time we have simply taken a shower1, grabbed lunch on-the-go, made dinner and then collapsed on the couch after doing the dishes2, we’ve likely come into contact with a multitude of harmful substances. Naked to the human eye, ‘micropollutants’ - tiny man-made molecules that include antibiotic residues, synthetic hormones, pesticides, and industrial chemcials, such as per and polyfluoroalkyl substances (known as PFAS) - are lurking everywhere creating a planetary-scale health risk. This includes in places previously considered relatively untouched by humans, such as the Mariana Trench and Antarctica, PFAS varieties have been detected3. Conventional wastewater treatment does not remove these micropollutants and consequently they end up back in the natural environment and ultimately bioaccumulating at the top of food-chain, in us. Although at acute and small concentrations micropollutants are unlikely to have long-lasting health impacts, chronic exposures have been linked to a range of serious health conditions. PFAS chemicals, for example, have been linked to cancers, autoimmune disorders, male and female infertility, obesity and diabetes4,5. Meanwhile, overuse of antibiotics and disinfectants are accelerating antimicrobial resistance (AMR) not just in bacteria, but also in viruses, fungi and parasites6. Following a 2023 assessment, it’s now estimated that the safe planetary boundary for pollutants ("novel entities" in Figure 1) has been exceeded7, putting the stability of the Earth system at risk. Figure 1: We are now outside the safe operating space of the planetary boundary for pollutants (‘novel entities’)8 Left unaddressed, the human and economic costs of micropollution will be severe. UNEP for example estimate 10 million deaths annually due to AMR by 2050 – equal to the number of deaths from cancer in 20209. Meanwhile, the World Bank puts the cost of healthcare associated with AMR at around USD $1 trillion by the same timeframe10. The numbers reach even dizzier heights when PFAS enter the equation. It’s thought that the bill for related direct-healthcare and environmental remediation could be as much as $17.5 trillion across the global economy11. Thankfully, the legal and regulatory landscape is beginning to catch up. In early April 2024, the U.S. Environmental Protection Agency (EPA) introduced the first legally enforceable limits on certain PFAS-levels12 in drinking water. However, a systemic problem requires systemic action, meaning financial markets have a role to play too. WHEB’s role in managing the problem Reducing risk At WHEB, we have been addressing the risk of micropollution through our stewardship and engagement activities for over a decade. In recent years we have joined several investor initiatives to support different aspects of our work on the topic. In fact in 2023, c.6% of our engagement activities focused on topics related to micropollution: Though not a manufacturer of PFAS chemicals, MSA Safety use the chemicals in meeting regulatory water and oil resistance requirements in protective firefighter turn-out gear made. In light of regulatory and technological developments, we have sought to get the company to commit to a time-bound phase-out of the chemicals. So far this has been challenging due to its reliance on supplier R&D. Still, MSA Safety has actively been working with the International Association of Firefighters to support the PFAS Alternatives Act, which would secure federal funding to support innovation. Since 2021, we have been leading a collaborative engagement with Ecolab via ChemSec’s Investor Initiative on Hazardous Chemicals. Ecolab’s cleaning products and services enable better water and energy efficiency in a range of downstream industries. However, a small number of its products contain substances of very high concern (SVHC). Here we have sought to secure a commitment from the company for a time-bound phase-out of SVHCs, as well as improved product circularity and better marketing of its safer alternative products13. Along with our partners in the Investors for Sustainable Solar14 initiative, we have been encouraging solar pv manufacturer First Solar on the safe use of Cadmium Telluride, a heavy metal, in their panels as well as on the use of alternatives to other toxic chemicals (such as in solvents) that are used in the manufacturing process for solar panels. We also believe that investors can, and should, utlise policy advocacy as a complementary method to direct company engagement. WHEB is therefore in the process of joining the Investor Action on AMR Initiative15. We hope this initiative will further support investor efforts to address AMR globally, and complement our own direct engagements. Empowering solution providers As impact specialists our investments support companies providing solutions to sustainability challenges, including those helping to tackle micropollution. Recent regulatory developments, such as with the US EPA, will likely benefit portfolio holdings that provide the technologies to address micropollution in its various forms. These stocks include: In short, WHEB’s efforts to address micropollution span various fronts: strategic investments in companies providing solutions, direct engagements with companies, bolstered by the coordination and expertise of relevant initiatives and policy advocacy . Through these channels, we continue to actively address the problem of micropollution with an approach that underscores our commitment to positive impact. WHEB: Stewardship in the Spotlight: Managing micro-pollution

WHEB: Cybersecurity – ESG or impact?

WHEB: Cybersecurity – ESG or impact?

(https://www.whebgroup.com/our-thoughts/cybersecurity-esg-or-impact)

Cybersecurity is becoming an increasingly prominent topic. The World Economic Forum published its Global Risks Report for 2024 and cyber-attack was ranked the 5th “most likely to present a material crisis on a global scale in 2024”. 1 For private sector stakeholders and governments, it ranked 3rd.

The cost of cyber-attacks is rising. The global cost of cybercrime damage is expected to hit $10.5 trillion annually by 2025, up from $3 trillion in 2015.2Lloyd’s of London estimate that a major global cyber-attack has the potential to trigger $53bn of economic losses, equivalent to a natural disaster the scale of superstorm Sandy.3

The frequency is also increasing. Research by Check Point, a major US cybersecurity company, showed that ransomware attacks reached an all-time high in 2023 with 10% of organisations worldwide targeted, a 33% increase on 2022.4

It’s clear that companies need to be considering cybersecurity as part of ESG. Intangible value, including digital assets like software and customer data, now represents 90% of the asset value of organisations. 5 That demonstrates that cyber-attacks present a material threat to the value of a company.

But should we go further and consider it as part of impact?

Cybersecurity and the environment

At WHEB, we define impact as products or services providing solutions to key sustainability challenges. To qualify, we would need to establish that cybersecurity is addressing an aspect of sustainability.

Looking first at the UN Sustainable Development Goals, there isn’t a goal that deals explicitly with cybersecurity. However, considering the definitions of a few of them there are reasons to believe that cybersecurity could be a contributing factor to achieving a number of goals:

Goal 6: Ensure availability and sustainable management of water and sanitation for all.

Goal 7: Ensure access to affordable, reliable, sustainable and modern energy for all.

Goal 9: Build resilient infrastructure, promote inclusive and sustainable industrialisation and foster innovation.

Goal 11: Make cities and human settlements inclusive, safe, resilient and sustainable.

The increasing use of digital and connectivity tools in each of these areas creates significant cybersecurity risks. There are numerous examples of energy infrastructure being targeted.6 Hackers have also targeted water treatment facilities in the US and Australia.7

The energy transition relies heavily on digital technologies and interconnectedness. As we wrote in a recent article, modernisation of the grid is critical for managing the increasing contribution of renewable energy and greater electrification. Attackers are increasingly targeting these operational technologies and in 2021 a survey of cybersecurity experts identified the energy sector as the most likely to suffer attacks on control systems.8

In his recent cybersecurity strategy paper, President Biden included a specific objective, “secure our clean energy future”.9 This feels like a clear demonstration of the importance of the issue to sustainability outcomes.

Cybersecurity and health

Digital technologies also increase vulnerability in other areas of sustainability, such as health. In 2017, the US Food and Drug Administration recalled 500,000 pacemakers due to the risk of hackers altering the patient’s heartbeat. In 2020 a hospital in Germany was forced to close its emergency department after a ransomware attack.10

The attacks are growing in scale. In February this year, a division of UnitedHealth Group in the US was the subject of a cyber-attack that left healthcare providers unable to fill prescriptions or get reimbursement for insurers. 11 A survey by the America Hospital Association found that 95% of hospitals experienced disruptions from the attack and 74% reported impacts to direct patient care.12

Technology adoption in healthcare is increasing rapidly, whether through wearable devices, hospital equipment or patient data records. That data is being used more widely too. Artificial Intelligence (AI) is a growing topic within healthcare, and high-profile AI companies like Nvidia are investing significant amounts in the industry.13

Cybersecurity and AI

The relationship between AI and sustainability is complex. What is clear is that AI is likely to increase the volume and heighten the impact of cyber-attacks.14 One emerging area is the spread of disinformation, which creates risks to elections and social cohesion.

In Slovakia’s recent election an AI-generated fake video circulated of a candidate discussing plans to manipulate the election, including buying votes15 Elections are vulnerable to a range of technological threats, including hacking, data breaches and more sophisticated forms of manipulation such as deepfakes and AI-generated disinformation.16

There will be over 40 national elections this year covering over 50% of global GDP, including the US and UK. In the US the government’s cybersecurity agency has published a Cybersecurity Toolkit to Protect Elections. One of the recommendations is the implementation of advanced technologies to detect and mitigate potential threats.

Cybersecurity and impact

At WHEB, we are in the early stages of exploring the topic of cybersecurity. But we do think there is a case for categorising it as a sustainability challenge. The challenge is a multifaceted one, and touches on many of our existing themes. The cost of ignoring the challenge is increasing, affecting more companies and more individuals every year.

Our next question is what are the solutions? This will involve looking at cybersecurity providers through the lens of our impact engine analytical framework. We are focusing on two areas where we think companies can have positive impact. First are companies providing products or services that have a differentiated outcome relative to the existing standards. Second are companies focused specifically on protecting the safety of individuals, for example through identity management software. This effectively widens the definition in our existing Safety theme beyond physical safety.

The world was slow to identify and act on existing environmental and social challenges. The consequences of that are now being felt. We hope cybersecurity will be different. And we think that we as impact investors have role to play in opening up the conversation on cybersecurity and starting to look more closely at solutions.

WHEB: Schneider Electric – spurring decarbonisation

WHEB: Schneider Electric – spurring decarbonisation

(https://www.whebgroup.com/our-thoughts/schneider-electric-spurring-decarbonisation)

Schneider Electric is a global leader in electrical products and systems used in energy management and automation. The company recently hosted its Capital Markets Day at the Tottenham Hotspur Stadium, a great case study for sustainable buildings. Schneider Electric partnered with Tottenham as the energy management supplier for its state-of-the-art stadium, which in 2021 hosted the first net zero football match, #GameZero.

To help the club deliver its sustainability goals, the stadium embedded Schneider’s EcoStruxure platform. The system combines electrical hardware with software to digitise and simplify electrical distribution systems. It enables analytics which feed into efficiency improvements, predictive maintenance, and safety. It also embeds cybersecurity tools which, as we wrote about here1, are becoming increasingly critical to green infrastructure.

Building sustainability

Building emissions account for over a quarter of global emissions2. While many solutions addressing renewable and efficient technology have emerged, the sector needs to do more to align with Net Zero 2050. One increasingly prevalent headwind is the perceived cost of the transformation, which was also a topic we covered recently in a blog post. A prominent example in the UK last year, was Rishi Sunak rowing back on green targets he said would impose a cost on consumer.3

In a quantitative study of building decarbonisation technologies, Schneider Electric suggests that one solution to the cost problem is increasing digitisation. This allows more flexible management of resources, for example planning usage to match periods of higher electricity supply or feeding excess capacity back to the grid from storage technology. This is particularly important as the share of renewables grows because supply becomes increasingly variable.

What’s great about the Schneider story is that the same technology can have benefits that go beyond environmental. EcoStruxure for Healthcare is one example delivering a wide range of benefits and Moorfields Eye Hospital is a good case study. The building is over a century old and EcoStruxure allowed Moorfields to integrate multiple systems and provide critical environment and power information essential to patient safety during surgeries. This led to reduced operating expenses and improved staff productivity, both valuable at a time when the health system is under such pressure.

Grid infrastructure

Another emerging area of interest for us is Schneider’s role in addressing the challenges facing the grid in the shift to electrification. We wrote about the topic in a previous article.

Schneider’s grid project with Enel illustrates how the company is contributing to solving problems such as the supply-demand imbalance and the increasing use of electricity. Enel is Italy’s largest power company and has the second largest installed generation capacity in Europe. Thanks to Schneider’s grid solutions, Enel has access to more accurate data and a system that can predict the impact of generation peaks as well as streamlining energy production. In combination that’s resulted in savings of roughly 75,000 tCO2 equivalent per year, 4 the equivalent of over 13,000 homes’ annual electricity use.5

Impact measurement

As well as being a leader in sustainable technology, we see Schneider as a leader in impact measurement and reporting. The company has developed the Schneider Sustainable Impact (SSI) program with six long-term positive impact commitments backed by 11 key indicators. Schneider also publishes a comprehensive methodology to measure emissions savings. This has several parallels with our own impact engine methodology, including a detailed analysis of what the relevant baseline for comparison should be.

Schneider is taking its expertise and deploying it with customers. The company recently published a framework for sustainability reporting for data centres. The aim is to help data centre customers develop key metrics and priorities for mitigating negative climate impacts. With the exponential growth in data centres this is becoming an increasing issue – they already account for almost 2% of global emissions6.

Schneider’s business touches a wide range of sustainability topics and we think the company is well placed to drive significant positive impact. Their technology leadership in these areas also supports the company’s ability to grow faster than the market while delivering attractive returns. Schneider is a great example of an investment thesis supported by positive impact, which is exactly what we look for in our portfolio.

Experian: Sustainability & SDG contribution roadshow (for investors & analysts) (21 May | 10 & 13 June | 31 July)

Experian: Sustainability & SDG contribution roadshow (for investors & analysts) (21 May | 10 & 13 June | 31 July)

Experian: Sustainability & SDG contribution roadshow (for investors & analysts) (21 May | 10 & 13 June | 31 July)

Experian’s sustainability-focused investor roadshows this year will focus on how their innovative products help improve the financial health of millions of people around the world and support financial inclusion for underserved and diverse populations. It will also introduce their new positive social impact framework which will be used in future to quantify how many people their products are helping thrive on their financial journey.

Sustainable investors and SRI/ESG analysts are invited to join meetings with company management to discuss:

- an update on the company’s products and programmes for financial health which contribute to UN SDGs 1, 8 & 9. (No poverty; Decent work & economic growth; Industry, innovation & infrastructure).

- an introduction to the new positive social impact framework

- wider aspects of the company’s ESG strategy and performance.

Analysts and investors to join the following events on Experian’s regular sustainability / ESG roadshow:

- Briefing call for ESG ratings agency analysts (Tues 21 May & 15:00 (London))

- Company participants: Evelyne Bull (Director, Investor Relations) & Melissa Goncalves Ferreira (Global Head of Sustainability)

- RSVP via SRI-Connect here or

This email address is being protected from spambots. You need JavaScript enabled to view it.

- 1-on-1 and small group meetings for investors (10th and 12th June)

- Company participants: Evelyne Bull, Charlie Brown (Company Secretary), Abigail Lovell (Chief Sustainability Officer), Melissa Goncalves Ferreira

- RSVP

This email address is being protected from spambots. You need JavaScript enabled to view it.

- Briefing call for ‘sell-side’ sustainability analysts Weds 31 July 15:00 (London))

- Company participants: Evelyne Bull, Nadia Ridout-Jamieson (Chief Communications Officer), Charlie Brown

- RSVP via SRI-Connect here or

This email address is being protected from spambots. You need JavaScript enabled to view it.

This briefing should be of interest and relevance to:

- ESG research and ratings analysts covering the company and also to

- analysts responsible for identifying sustainability thematic opportunities – notably social thematic opportunities and those related to the UN Sustainable Development Goals.

HSBC: Climate Solutions Playbook 2024 - Investing in the transition

HSBC: Climate Solutions Playbook 2024 - Investing in the transition

- As the world continues to warm, the focus on clean investments is also soaring...

- ...leading to an increasing relevance of companies that operate in this domain

- We use our proprietary HSBC Climate Solutions Database to create thirteen thematic climate stock screens

Clients of HSBC Global Research can access the full report via the HSBC Global Research website or by contacting Wai-Shin Chan

Investments in global energy transition, land-use and other clean technologies are growing at a brisk pace. However, they need to accelerate further into trillions of dollars per year to meet global climate goals and to make economies more resilient to adverse climate change impacts. Effective execution of climate ambitions could support clean-tech sectors, and corporates that operate in this space could benefit from rising investments. In this report, we use our proprietary HSBC Climate Solutions Database to present 13 stock screens across 10 broad strategies aligned with various thematic ideas. Overall, screens offer around 340 stock names which are involved in providing climate solutions - both mitigation and adaptation.

Klement on Investing: Do ESG fund managers have ESG skill?

Klement on Investing: Do ESG fund managers have ESG skill?

We know that active fund managers can only beat a benchmark if they have skill in selecting stocks and/or timing the market. But we also know that skill is a rare commodity and the majority of fund managers do not have skill. But what about ESG funds and their skill in picking stocks that improve their ESG credentials over time?

A team from the University of Virginia decided to investigate if there is such a thing as ESG skill and if it translates into better performance for ESG funds. To do this, they took inspiration from the conventional measure of skill, namely the ability to buy stocks when the price is low and sell them when the price is high. Similarly, they defined ESG skill as the ability of fund managers to buy stocks before their ESG ratings are upgraded (i.e. when the ESG performance is low) and sell them when the ESG performance is high.

Using three different ESG ratings methodologies, the study found that close to 50% of ESG fund managers have some form of ESG skill in the sense that they are on average able to buy stocks before their ESG ratings are being upgraded. But that skill is tiny, and the picture becomes much more selective if one is looking for statistically significant levels of skill. If one wants to have a 95% probability that the manager has ESG skill only about 5-10% of managers qualify.

Accela: Oil and Gas Majors’ 2024 AGMs - The low-carbon investment gap

Accela: Oil and Gas Majors’ 2024 AGMs - The low-carbon investment gap

(https://www.accelaresearch.com/research/agm2024sectorreport)

"Accela’s annual pre-AGM in-depth on Global Oil and Gas Majors, assesses the achievability of and the investment needed to meet net carbon intensity targets.

This report launches Accela’s Transition League Table, a new framework to rank European major's oil and gas transition strategies, incorporating the most critical elements of transition performance.

In our latest analysis, we delve into the performance and ambition of the transition plans for 5 European and 2 Australian oil and gas majors.

Our analysis finds minimal progress in reducing net carbon intensity (declining on average ~4% on FY19-23) compared with targets of 15-20% (FY19-23), with European majors needing to deliver ~US$300 bn of investment between now and 2030 to meet existing targets."

GFI: State of the Industry Reports (Alternative Proteins)

GFI: State of the Industry Reports (Alternative Proteins)

|

"For the past five years, GFI’s global State of the Industry Report series has provided a macro lens on the alternative protein landscape’s evolution, helping stakeholders view recent news developments in a more complete context. |

Robeco: Energy storage – the next challenge in the energy transition

Robeco: Energy storage – the next challenge in the energy transition

Without energy storage, renewable energy’s potential can’t be fully harnessed, putting net-zero targets in jeopardy. But trade-offs and complexities in energy markets mean only a few players stand to benefit from the expansion of storage capacity.

Summary

- Renewable energy’s share of the energy mix expanding

- Renewables are clean and abundant but also unreliable

- Lithium batteries to dominate storage and grow market share

WWF: Palm Oil Scorecard 2024

WWF: Palm Oil Scorecard 2024

(https://palmoilscorecard.panda.org/)

'In 2024, the urgency to combat climate change peaks. The palm oil industry, a major player, demands swift action. The 2024 Palm Oil Buyers Scorecard by WWF reveals a sobering truth: palm oil buyers are yet to step up to the challenge, leaving the fate of our planet hanging in the balance. The Scorecard is our wake-up call, emphasising the need for bold, transformative measures for a sustainable future.'

NB: scorecard contains a number of quoted company brands

Centrica: People & Planet Update 2023

Centrica: People & Planet Update 2023

(https://www.centrica.com/media/ag0mxnig/people-and-planet-incl-tcfd-ar-2023.pdf)

Centrica: People & Planet Update 2023

Centrica's latest Annual Report contains a people & planet section, covering:

- Foundations - Customers, colleagues, communities and ethics

- Non-financial and sustainability information

- Material risks and opportunities

- Performance metrics

HSBC: Climate Investment Update - EU Green Deal: Deforestation regulation is under fire

HSBC: Climate Investment Update - EU Green Deal: Deforestation regulation is under fire

HSBC: Climate Investment Update - EU Green Deal: Deforestation regulation is under fire

- Some EU member states are attempting to delay or possibly scale back the EUDR; trading partners are also critical

- The EU has already delayed the country risk classification system and most industries and countries are underprepared

- We think there are indications that the full implementation of the EUDR will be delayed; cattle and cocoa industry will gain

Clients of HSBC Global Research can access the full report via the HSBC Global Research website or by contacting Wai-Shin Chan

ISS ESG: The Latest in ESG and Stewardship Regulation – April 2024

ISS ESG: The Latest in ESG and Stewardship Regulation – April 2024

The latest regulatory developments related to ESG and stewardship worldwide.

This monthly bulletin produced by ISS STOXX’s Regulatory Affairs & Public Policy group provides a review of regulatory developments that may be relevant to investors and companies.

IOSCO

International Organization of Securities Commissions (IOSCO) Chair Gives Keynote Address at IFRS Sustainability Symposium

On February 22, IOSCO Board Chair Jean-Paul Servais gave a keynote address at the IFRS Sustainability Symposium, discussing IOSCO’s endorsement of ISSB’s first sustainability disclosure standards and praising international adoption of the standards. Jean-Paul Servais also affirmed that “IOSCO is committed to collaborating with the ISSB and other global stakeholders to deliver a sound capacity building program to support the wider roll-out of sustainability disclosures.”

SBTi

SBTi Releases Reports on Design and Implementation of Beyond Value Chain Mitigation

On February 28, the Science Based Targets initiative (SBTi) released two new reports to aid the design and implementation of beyond value chain mitigation (BVCM) strategies. BVCM strategies do not affect companies’ Scopes 1, 2, or 3 emissions; they are another method to allow companies to “help accelerate the global net-zero transformation by enabling other economic and social actors to avoid, reduce or remove GHG emissions.” The first report – the “Above and Beyond” report – explores the creation, functionality, and implementation of BVCM strategies; meanwhile, the second report – the “Raising the Bar” report – explores barriers and incentives to the adoption of BVCM strategies.

Japan

Japanese Ministry of Environment and World Business Council Announce Collaboration on Global Circularity Protocol

The Japanese Ministry of Environment and the World Business Council for Sustainable Development announced their collaboration in developing the Global Circularity Protocol during the 6th UN Environment Assembly by signing a Memorandum of Cooperation. The announcement affirmed the continued cooperation on the Protocol that aims to promote circular business models globally through providing companies with a standard Corporate Performance Accountability System (CPAS) for Circularity; harmonizing circularity methodologies; adding accounting metrics for corporate-level circularity performance; and developing Science-Based Targets for Circularity. Simultaneously, the Protocol also aims to guide governments on regulation frameworks that would promote circularity.

Singapore

Deputy Prime Minister of Singapore Affirms Commitment to Combatting Climate Change at NUS Sustainable and Green Finance Institute’s Sustainability Summit

In his remarks on March 21 at the National Union of Singapore Sustainable and Green Finance Institute’s (SGFIN’s) Sustainability Summit, Mr. Heng Swee Keat, the Deputy Prime Minister of Singapore and the Coordinating Minister for Economic Policies, reaffirmed Singapore’s commitment to a Net-Zero-by-2050 target. The Deputy Prime Minister emphasized Singapore’s Green Plan 2030 – a sustainable development roadmap – as well as efforts by the Singapore Exchange to progressively introduce “mandatory requirements for climate-related disclosures as part of sustainability reporting by Singapore-listed companies.” The Deputy Minister also stated that the government is considering policy innovations, including carbon pricing, to promote sustainability.

South Korea

Korean FSC Holds Meeting with Investors to Discuss the Korean Value-up Program

On March 14, the Korean Financial Services Commission (FSC) held a meeting with 10 large institutional investors to reveal and promote efforts to improve investor participation in the Korean Value-up Program. The Value-up Program aims to increase corporate value and address the ‘Korean discount’ — a phenomenon where South Korean companies tend to have lower valuations than global counterparts due to geopolitical and governance reasons — through three main principles. The third principle focuses on “promoting shareholder values in corporate management”; the Program recommends achieving this goal through promoting shareholder-friendly corporate practices. Concurrently, the Korean Stewardship Code for Institutional Investors has been updated to encourage investors to engage with companies and promote voluntary measures in line with the Program; one such amendment to the Code requires investors to actively monitor how companies are attempting to implement the Program. Lastly, the FSC revealed in its meeting with investors details about the new Value-up Index being developed by the KRX in alignment with the Program.

Korean FSC Holds Meeting with Heads of Major Commercial Banks to Discuss Policies Intended to Boost Climate Finance

The Chairman of the FSC, as well as other government officials, met with the heads of major commercial banks to promote policies intended to boost climate finance. The FSC told banks that, amidst the challenges presented by climate change, the role of banks in the transition to a low-carbon economy will be enhanced. The FSC’s new initiatives aim to funnel investment from major financial institutions and venture capital firms to renewable and clean energy industries and climate technology. During the meeting, the Korean Ministry of Environment announced new low-carbon measures, including upgrading the Korean Green Taxonomy (K-Taxonomy); increasing green investment to as much as KRW30 trillion by 2027; and making improvements to South Korea’s emissions trading scheme.

Malaysia

Securities Commission Malaysia Releases Draft Governance Code for MSMEs

The Securities Commission Malaysia (SC) is seeking feedback on their draft Governance Code for Micro-, Small, and Medium-sized Enterprises (MSMES). The Small and Medium-Sized Enterprises (SMEs) Governance Working Group developed the Code to promote good governance practices among MSMES, in alignment with the 12th Malaysia Plan and the National Entrepreneurship Policy 2030. Complementing MSME guidance in the Simplified ESG Disclosure Guide and the ESG Quick Guide, the voluntary Code gives size-proportionate recommendations on good governance practices, and proper accountability mechanisms for the management of sustainability risks and opportunities; the recommendations of the Code are aligned with the principles of the Malaysian Code on Corporate Governance.

Bursa Malaysia to Serve as Chair on Stock Exchange Collaboration to Develop ASEAN-Interconnected Sustainability Ecosystem

On February 15, Bursa Malaysia, the Indonesia Stock Exchange (IDX), the Stock Exchange of Thailand (SET), and the Singapore Exchange (SGX Group) announced their collaboration on the development of the ASEAN-Interconnected Sustainability Ecosystem (ASEAN-ISE), with Bursa Malaysia serving as Chair. The exchanges aim “to advance ASEAN’s sustainable development through the implementation of common ESG metrics in their respective data infrastructures.” Each of the participating exchanges has committed to adopting and implementing the “ASEAN Exchanges Common ESG Metrics” when they are fully developed. The primary goals of the exchanges’ collaboration are creating an integrated ESG ecosystem; enabling exchanges to achieve economies of scale with fit-for-purpose efficiency solutions; and empowering exchanges to maximize the business value of ESG-compliant companies, including through requiring quality disclosures, connecting supply chains to ESG-oriented investment capital, and strengthening the infrastructure needed for cross-border trade flows.

Australia

ASIC Publishes Article for Small Businesses on Impact of Mandatory Climate Disclosure

The Australian Securities & Investments Commission (ASIC) published an article informing small businesses of upcoming climate disclosure regulation in Australia and how it may impact them. The Australian government has proposed introducing regulation that would mandate climate disclosure for financial institutions, large businesses, and businesses that meet two of the following criteria: has a consolidated revenue of A$50 million or more; has consolidated gross assets of A$25 million or more; and has 100 or more employees. Small businesses will be subject to certain reporting requirements through the Scope 3 reporting requirements of large businesses, provided that these requirements do not impose undue costs. ASIC also provided small businesses with guidance on how to avoid greenwashing charges based on false or misleading reporting or marketing claims.

ASIC and APRA Release Final Rules and Guidance for Implementation of Financial Accountability Regime

ASIC and the Australian Prudential Regulation Authority (APRA) released the final rules and guidance to aid the implementation of their Financial Accountability Regime (FAR). FAR aims to “improve the risk and governance cultures” in key financial industries by imposing a stronger accountability framework for regulated entities in banking, insurance, and superannuation, as well as relating to directors and executives within those industries. The latest guidance follows a public consultation and aims to clarify key regulatory and transitionary provisions.

Read the full report at: https://insights.issgovernance.com/posts/the-latest-in-esg-and-stewardship-regulation-april-2024/

ISS ESG: Ready, Set, Regulation

ISS ESG: Ready, Set, Regulation

Regulators globally are requiring companies to disclose their greenhouse gas (GHG) emissions. For companies in some industries, Scope 1 and 2 emissions – covering, respectively, emissions from direct fuel use and from acquired energy – will cover most relevant emissions caused by their activities, and these are relatively simple to calculate and disclose.

For most companies in the financial sector, though, the bulk of relevant emissions are categorised as Scope 3 indirect emissions, specifically, financed emissions. These are much more problematic to calculate or estimate. Regulators, however, are likely to demand that companies disclose these emissions; otherwise, reporting will be limited to emissions that are marginal to the real impact these companies have.

Attention to Scope 3 emissions is likely to grow, as the financial sector has a key role to play in financing a transition to a low-carbon economy. The financial companies can play this role both by reducing their financing of carbon-intensive industries and providing the capital required by sustainable alternatives.

ISS ESG assesses the readiness of financial companies to disclose and mitigate their carbon impact. This post uses data from the ISS ESG Corporate Rating and from ISS Economic Value Added (EVA) to assess the readiness of financial companies, across different markets and regulatory jurisdictions, to meet this challenge.

Various areas show marked differences in how prepared their financial companies are to meet increased disclosure requirements. Some jurisdictions—e.g., the Netherlands, France, Taiwan—exhibit high preparedness, while others—e.g., the United States and India—exhibit low readiness in anticipation of new regulatory requirements and expectations.

Companies that better disclose financed emissions tend to perform better in demonstrating strategies to mitigate their GHG impact and increasing financing of low-carbon alternatives. These companies also demonstrate stronger financial performance, which suggests a positive correlation between climate responsibility and strong profitability.

Read the full report at: https://insights.issgovernance.com/posts/ready-set-regulation/

ISS ESG: Grid Bottlenecks and the Clean Energy Transition: Lessons Learned from China

ISS ESG: Grid Bottlenecks and the Clean Energy Transition: Lessons Learned from China

Grid bottlenecks have become one of the most significant challenges to the global clean energy transition. In 2023, some news reports indicated that countries with ambitious decarbonization and energy transition plans are facing serious hurdles to connect solar and wind power to consumers, largely because of insufficient grid infrastructure and capacity.

These challenges are present in China. Despite leading in renewable energy development, China has experienced grid bottlenecks and serious renewable power curtailment as early as the mid-2010s.

One option for addressing bottlenecks is developing ultra-high voltage power lines, grid-scale storage, and smart grids. Investors looking to promote the clean energy transition may be interested in pursuing opportunities in these key industries, and several ISS solutions such as ESG Corporate Rating, SDG Impact Rating, or SDG Solutions Assessment can help them in this area.

Expanding Renewable Energy Capacity but Limited Consumption

A World Leader in Renewables

China has been a leader in renewable energy development, topping the list of the world’s total renewable energy capacity generators as early as 2006. That year China had 135.5 GW capacity, with the United States in second place at 124.7 GW.

The capacity gap between the world’s first- and second-largest developers of renewable energy has grown even more prominent over the last two decades. In 2022, China’s total renewable energy capacity reached 1160.8 GW, nearly 3.3 times the United States’ capacity of 351.7GW. In solar and wind power expansion specifically, China has had the world’s largest solar power electricity generation capacity since 2015 and the largest wind power generation capacity since 2016.

Many wind and solar power projects were developed in northern China, which has the most abundant wind and solar energy resources, with the support of local governments intending to stimulate economic growth, generate tax revenues, and create job opportunities. Local government support for wind and solar power developers, combined with the rollout of favorable policies and generous subsidies from China’s central government, resulted in a surge in renewable power capacity.

Read the full report at: https://insights.issgovernance.com/posts/grid-bottlenecks-and-the-clean-energy-transition-lessons-learned-from-china/

Korea Investment Corporation: Sustainable Investment Report 2023

Korea Investment Corporation: Sustainable Investment Report 2023

(https://www.kic.kr/_custom/kic/_common/board/download.jsp?attach_no=46333)

Korea Investment Corporation latest annual Sustainable Investment report covers key areas of their activities, including:

- ESG Integration - ESG Integration, ESG Review and ESG Program

- Climate Change - Carbon Footprint, Climate Scenario Analysis and Risks

- Stewardship Activities - Proxy Voting, Shareholder Engagement, and Voting Cases

- Partnership

PRI: PRI Awards 2024

PRI: PRI Awards 2024

(https://www.unpri.org/showcasing-leadership/the-pri-awards-2024/12268.article)

"The PRI Awards 2024 are now open entries until 14 June 2024. The details below should provide all the information you require to plan a submission and submit your entry.

We will welcome all types of entries covering different activities and issues. If you have further questions, please contact

SABIC: Integrated Annual Report - Chemistry that shapes tomorrow

SABIC: Integrated Annual Report - Chemistry that shapes tomorrow

(https://www.sabic.com/en/Images/SABIC-Integrated-Annual-Report-2023-EN-Updated_tcm1010-42927.pdf)

SABIC's latest Integrated Report covers key areas of their ESG activities, including:

- Environmental, Health, Safety & Security

- Climate change & resource efficiency

- Sourcing

- People & societal impact

Stora Enso: Annual Report 2023

Stora Enso: Annual Report 2023

Stora Enso's latest Annual Report covers Sustainability on pages 35-82, key areas covered include:

- Sustainability targets

- Climate change: emissions

- Sustainable forestry and biodiversity

- Circularity & Product stewardship

- Materials, residuals, and waste

- Energy & Water

- Employees, Safety, Human rights & Community

- Sustainable sourcing

Planet Tracker: The Global Plastic Pollution Treaty negotiations – what financial institutions should watch out for…

Planet Tracker: The Global Plastic Pollution Treaty negotiations – what financial institutions should watch out for…

Planet Tracker: The Global Plastic Pollution Treaty negotiations – what financial institutions should watch out for…

Curbing plastic pollution will be on the agenda next week when Ottawa hosts the fourth round of negotiations (INC-4) to develop an international legally binding instrument on plastic pollution, including in the marine environment, from 23rd to 29th April 2024.

This is the next stage in the negotiations to develop a global plastics treaty before the end of 2024.

Countries are expected to discuss the provisions of the revised Zero Draft – i.e. an initial attempt to gather high-level thoughts on an issue – as well as agree the rules of procedure.

The latter has been by a small handful of countries to insist on a consensus-based approach for voting, therefore allowing a single country veto rather than permitting a majority-based system.

This is not only making decision-making difficult as contentious issues are sidelined, but it also consumes valuable negotiating time.

Currently, the Zero Draft contains several options that delegates are expected to use as a basis for negotiations, including the scope of the treaty, its implications and the means of implementation.

Read our latest blog for the five main areas that financial institutions should keep in mind.

Terra Alpha: 2023 Impact Report: Enabling a Sustainable Planet for Society

Terra Alpha: 2023 Impact Report: Enabling a Sustainable Planet for Society

(https://terraalphainvestments.com/wp-content/uploads/2024/03/TAI-2023-Impact-Report-1.pdf)

Terra Alpha's fourth Impact Report details its progress towards sustainability across:

- Portfolio - investment process and portfolio construction

- Corporate Engagement - engagement directly with portfolio companies including proxy voting, thematic campaigns across companies, and company specific interaction

- Thought Leadership - thought leadership and advocating with collaborative efforts on the policy front

CWR: China ICT running dry?

CWR: China ICT running dry?

The rise of AI & climate risks amplify existing water risks faced by thirsty data centres

CWR releases a new report, “China ICT running dry? The rise of AI & climate risks amplify existing water risks faced by thirsty data centres”. The report reveals 4.3mn data centre racks in China consume around 1.3bn m3 today but can rise to >3bn m3 by 2030. This will put pressure on already stressed water resources, especially as the rise of AI & chatbots could see water use surge by a shocking 20x.

For perspective, ~1.3bn m3 is 1.9x the water use for households & services in Tianjin, a city of 13.7mn people… but with data centre growth plus AI, this could explode to more than 500mn people!

Clearly, this doesn’t bode well for China ICT as it is already highly exposed to various water risks. Of the 4.3mn national data centre racks:

- 46% are located in regions as dry as the Middle East;

- At least 41% are located in regions that are highly prone to drought while at least 28% are in areas highly prone to floods + at least 1/5 are very prone to both;

- 56% are located in coastal regions vulnerable to storm surge & sea level rise; and

- >75% lie in 3 river basins – Yellow, Yangtze & Pearl = vulnerable to basin & regulatory risks.

Bloomberg: Elon Musk’s Tesla Bait-and-Switch Is Getting Old

Bloomberg: Elon Musk’s Tesla Bait-and-Switch Is Getting Old

The EV company keeps pushing its “next phase of growth” message, but it’s getting harder to look past a slump in vehicle sales and its unexciting lineup.

In case you didn’t know that Tesla Inc. is on the cusp of a new wave of growth, it is now slashing its workforce by more than one-in-ten. It’s all there in the memo.

Chief Executive Elon Musk informed the ranks this weekend that more than 14,000 of them — based on year-end 2023 figures — would be leaving the electric vehicle manufacturer forthwith. The announcement is one part regret, three parts optimism. The phrase “next phase of growth” appears up top and in the kicker, with a derivative of it somewhere in the middle, too. This is all quite normal corporate stuff: Companies doing big layoffs must emphasize the leaner, fitter organism that will emerge. But this is Tesla at an interesting moment in its development, so the context matters.

ISS ESG: Advancing Sustainability: The Drive Towards Hydrogen-Based Technologies

ISS ESG: Advancing Sustainability: The Drive Towards Hydrogen-Based Technologies

Addressing climate change requires reducing greenhouse gas (GHG) emissions, especially carbon dioxide (CO2) emissions, which are the primary cause of global warming. The goal of reducing GHG emissions makes moving away from fossil fuels to renewable energy sources essential.

Hydrogen-based technologies offer the possibility of a clean energy source for transportation, electricity generation, and industry. Governments are developing regulations for hydrogen technologies and have adopted policies to encourage renewable hydrogen development.

Many businesses, especially in the energy sector, are similarly investing in green hydrogen technologies. ISS ESG services, such as the ISS ESG Corporate Rating, can assist investors in tracking corporate performance on green hydrogen and other hydrogen-based technologies.

Green Hydrogen in the Transition to a Sustainable Energy Future

Unlike fossil fuels, which are finite and contribute to pollution and climate change, renewable energy sources such as solar, wind, tidal, and geothermal heat are sustainable and have minimal environmental impact. As renewable energy generation is not consistent, addressing sudden spikes in energy demand is challenging. Energy storage and hydrogen technologies may offer solutions to this problem.

A region with a highly renewable grid requires short-term bursts of power, such as those generated by hydropower or batteries. Hydrogen can address storage requirements to cover periods, ranging from a few hours to a few days, when wind and solar are not accessible, and hydropower and batteries are depleted.

Hydrogen, which is colorless and odorless in a pure gaseous state, is the most common chemical element in the universe. Despite its abundance, it is difficult to access and purify it, partly because natural hydrogen frequently occurs in subaerial and undersea environments such as mid-ocean ridges. Though the potential of natural hydrogen cannot be dismissed, significant research is needed to capitalize on this source.

As the purity of the hydrogen is an important factor in its end-use applications, hydrogen is often produced rather than extracted. Hydrogen can be produced through different methods. The most common types of hydrogen, and their methods of production, are as follows:

- Grey Hydrogen: Generated by steam reforming of natural gas or methane, a process that brings together natural gas and heated water as steam. This process produces CO2 as a by-product.

- Blue Hydrogen: Generated by the same steam reforming process as grey hydrogen, but with the addition of carbon capture, utilization, and storage (CCUS) to trap the CO2.

- Green Hydrogen: Produced by water electrolysis using renewable energy sources.

Other types of hydrogen include turquoise hydrogen, made by methane pyrolysis; pink hydrogen, produced by electrolysis using nuclear power; and brown/black hydrogen, produced through coal gasification.

Among these types, green hydrogen is the cleanest, although it is also water intensive: according to the International Energy Agency, production of a kilogram of green hydrogen requires nine liters of water. Blue hydrogen is also considered low-carbon hydrogen due to the inclusion of CCUS. The IEA reports that grey hydrogen is currently still the predominant type. Reaching the Net Zero Emissions by 2050 (NZE) scenario will likely require scaling up green hydrogen, though.

Verisk Maplecroft: Threats to food security increase in 135 countries – Europe registers largest uptick in risk

Verisk Maplecroft: Threats to food security increase in 135 countries – Europe registers largest uptick in risk

Threats to food security are rising globally as governments grapple with the fallout from fluctuating commodity prices amid a cost of living crisis and increased economic, geopolitical and environmental volatility, according to our latest research.

Our Food Security Index (FSI), which evaluates the availability, access and stability of food supplies in 186 countries, shows that 135 countries have seen an increase in risk since 2022-Q4, compared to 48 where the risk decreased. Only 13 countries fall within the low risk category of the latest edition of the FSI, the lowest number since the dataset launched in 2017.

Risks continue to run highest in parts of the developing world, with countries in Africa, Asia and the Americas most at risk. But the data – which also considers nutritional outcomes for each country’s population - highlights rising food insecurity even among rich nations, with Europe witnessing the largest increase in risk of any region. The likes of Australia, New Zealand and Canada have also seen an uptick.

iRIS Carbon: The Impact of ESG Disclosure Scores on Investor Perception and Financial Performance

iRIS Carbon: The Impact of ESG Disclosure Scores on Investor Perception and Financial Performance

The way investors assess firms has seen a radical change in the last several years. Environmental, Social, and Governance (ESG) aspects have become important indications of a company’s long-term health and resilience, surpassing traditional financial measurements. Corporate governance procedures, social responsibility, and environmental stewardship are just a few of the many topics covered by ESG.

ESG disclosure scores are becoming more and more important in influencing investor perception and promoting financial success as investors grow to understand the value of sustainability and moral behaviour. In this blog, we will look into the ways in which businesses can use ESG activities to gain a competitive edge and sustain growth as we delve deeply into the complex interplay between investor perception, financial performance, and ESG disclosure scores.

HXE Partners: How double materiality assessments can go beyond CSRD compliance

HXE Partners: How double materiality assessments can go beyond CSRD compliance

(https://hxepartners.com/how-double-materiality-assessments-can-go-beyond-csrd-compliance/)

The European Union (EU)’s Corporate Sustainability Reporting Directive (CSRD) aims to make corporate sustainability reporting more transparent, consistent, and standardized to help drive capital towards sustainable investment as part of the new Green Deal.

Companies subject to the CSRD will have to prepare a “sustainability statement” according to the new European Sustainability Reporting Standards (ESRS), with the first set of sector-agnostic standards having been adopted by the European Commission in July 2023. Sector-specific standards as well as standards for small- and medium-sized businesses and non-EU parent companies are still under development.

Additionally, specific implementation elements, such as filing deadlines and consequences of non-compliance, are still being finalized, as EU member states are in the process of transposing the directive’s requirements to national law by July 1, 2024. by July 1, 2024.

Impact Cubed: The Real Impact of the Top Three ESG Funds

Impact Cubed: The Real Impact of the Top Three ESG Funds

(https://www.impactcubed.com/post/the-real-impact-of-the-top-three-esg-funds)

We look at the ESG impact of the top three ESG funds by 2023 US inflow, and question whether they live up to their 'green' credentials.

The global financial market faced a lot of turbulence in 2022, and ESG funds were especially affected, as investors tried to avoid the perceived risk from ESG products to safeguard their wider investments. However, by the end of 2023, ESG funds had started to recover. Three ESG funds stood out, receiving the top net inflows of 2023.

A closer examination of these funds shows, however, a complicated story that institutional investors often have to navigate. We compare the actual impact of these top ESG funds, with Morningstar USA Market Extended Benchmark as a reference point, to see whether they live up to their climate credentials.

ISS ESG: Land Use and Management: Measurement and Impact

ISS ESG: Land Use and Management: Measurement and Impact

ISS ESG: Land Use and Management’s Impact on Key Environmental Risks

The two major environmental concerns dominating investor discussions today are climate change and biodiversity. The Stockholm Resilience Centre’s 9 Planetary Boundaries, the ‘natural’ limits within which humanity can survive and thrive, act as a reminder of the intricacies of both climate change and biodiversity, how they represent ‘interrelated processes within the complex biophysical Earth system’ and thus how each intrinsically impacts the other.

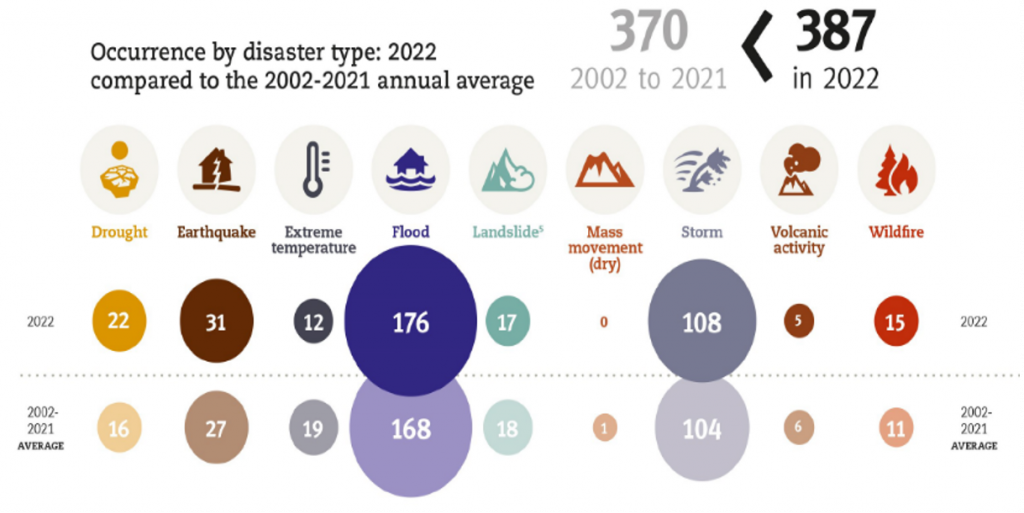

‘Climate Change’ is one of these planetary boundaries, and its global impacts on biodiversity, especially climate-related hazards, have increased both in terms of frequency and intensity. As of early October 2023, approximately one-third of 2023 had been 1.5°C higher than pre-industrial levels. Moreover, according to the international disasters database EM-DAT, the number of occurrences of floods, droughts, and wildfires in 2022 was greater than the average experienced over the previous 20 years (Figure 1). As a result, continued warming may well lead to a negative and potentially irreversible impact on biodiversity.

Figure 1: Climate Hazard Frequency, 2002-2021 vs 2022

Source: EM-DAT

Another planetary boundary that critically impacts both climate and biodiversity is ‘Land-System Change.’ However, there are different ways to actively limit these land-system changes, which currently contribute to higher GHG emissions. Limiting deforestation-related activities to reduce biodiversity loss, for instance, is also a key tool at humans’ disposal to decrease carbon emissions from the atmosphere. Implementing more sustainable agriculture practices, whether in relation to crops, livestock, or land management, is another one.

But how can investors monitor and measure the impact of Land Use when looking to mitigate these key environmental risks?

Read more at: https://insights.issgovernance.com/posts/land-use-and-management-measurement-and-impact/

ISS ESG: AI and the Labor Economy: It Still Takes Two (Labor & Capital) to Tango

ISS ESG: AI and the Labor Economy: It Still Takes Two (Labor & Capital) to Tango

ISS ESG: AI and the Labor Economy: It Still Takes Two (Labor & Capital) to Tango

The launch of ChatGPT ignited a race to measure the potential impact of artificial intelligence (AI) on the global labor market. Researchers pored over job classification systems to estimate the proportion of tasks that could be eliminated by AI agents, whose marginal costs approach zero. Several studies have concluded that a sizeable chunk of today’s work could eventually be done by machines.

History suggests the macroeconomic impact on employment and wage levels is highly uncertain. However, as companies drive AI adoption in the workplace, the biggest winners might be those that optimize the complementary nature of labor and capital.

Investors might want to search for opportunities not only among companies enabling AI-driven innovation but among those making strategic investments in human capital alongside those in technology. The metrics collected under the ISS ESG Corporate Rating suggest that systematic employee training and career development remain underappreciated among many companies.

Exposure to AI is Significant Across the Broader Labor Economy

Sensational claims are commonplace when AI and jobs are mentioned together: ‘AI Could Steal Over 80 Million Jobs in the Next 5 Years,’ or ‘300 Million Jobs Could Be Affected by Latest Wave of AI.’ Without additional context, these statements connote mass unemployment. Studies on the topic create a much more nuanced picture, while acknowledging the high degree of uncertainty in their estimates.

The OECD estimates that 27% of global jobs are at high risk of automation from AI and other technologies. Briggs and Kodani (2023) estimate that nearly 18% of work globally (and one-quarter of work in the United States and Europe) could be automated by generative AI alone. This is consistent with a recent study (2023) from the Pew Research Center and another by Sytsma and Sousa (2023) suggesting that 19% and 15% of Americans, respectively, are in jobs with high exposure to AI.

Further, according to Daugherty et al. (2023), an estimated 40% of U.S. working hours may be impacted by large language models (LLMs) more broadly. Routinized tasks may be automated away (e.g., credit authorization), while others may be augmented with AI-powered tools (e.g., biomedical engineering).