Profile achieved (industry-wide)

We are fully transparent about the profile achieved by organisations and individuals across our network and issue regular updates on industry visibility.

Here we list the buzzes and profiles that have been most viewed in the last 90 days.

For full details and rankings of which firms and individuals are most effectively developing their online profile in sustainable investment and corporate governance engagement on SRI-CONNECT, see Our reach; your opportunity.

Or you can request a personalised Industry Profile Report that analyses and benchmarks (vs peers) the activity and visibility of individual firms.

Most read research buzzes

(697) Guinness GI: The long-term opportunity for wind energy

Guinness GI: The long-term opportunity for wind energy

(https://www.guinnessgi.com/insights/long-term-opportunity-wind-energy)

"The wind industry quietly recorded another year of record installations in 2025. While other generation technologies such as solar and nuclear have dominated headlines in recent years, the wind industry has quietly been gathering momentum. With strengthening demand drivers, long-term political support in Europe and China, and attractive long-term economics, we believe that wind adoption will continue to grow."

(641) HSBC: Gamechangers: The next stage of AI’s impact on the economy

HSBC: Gamechangers: The next stage of AI’s impact on the economy

(https://www.business.hsbc.com/en-gb/insights/gamechangers-the-next-stage)

Almost every economics presentation or meeting over the past few years has had to include a mention or a question about AI – and rightly so. The impact of the technology on the economy has both been meaningful already and is set to increase in the coming years.

We’ve seen impacts on growth in the US via software investment and data centres, a boom in Taiwanese exports, and financial markets dominated by the winners and losers of AI.

But beyond the initial buildout, the second-round macro impacts in most of the world have been pretty small so far.

- We haven’t seen mass layoffs.

- We haven’t seen productivity spike.

- We haven’t seen our day-to-day lives transformed by AI quite yet.

(590) HSBC: Future transport: Ignore consumer preference at your peril

HSBC: Future transport: Ignore consumer preference at your peril

The transport sector is making some progress on decarbonisation, but it is slow and the outlook is tough. According to the UN, the sector accounts for roughly one-quarter of global greenhouse gas emissions.

Making transport clean(er) remains the central tenet of the industry.

... includes ...

- Road is key

- The headwinds to EV adoption, however, are clear and well-rehearsed

- Regulators have started to adjust to reflect this reality

- The road ahead

- For sea and air transport, the challenge remains the availability of alternative fuels

- Meanwhile, autonomous driving is gaining speed

(548) Transition Tapes: Harald Walkate - Rethinking sustainable finance narratives

Transition Tapes: Harald Walkate - Rethinking sustainable finance narratives

"‘Reference narratives’ are beliefs that spread contagiously “go viral”, self-reinforce. But what if the narratives shaping sustainable finance don’t fully reflect reality?

The latest thoughtful, jazzy episode of The Transition Tapes is called: The power of ‘Reference Narratives’: How the stories we tell about sustainable finance and the way we test the truth/reality of those narratives is fundamental to progress.

In this episode, I chat with Harald Walkate, Advisor on Financing Sustainability & Blended Finance: Route17 and Senior Advisor Blended Finance Lab at the LSE.

We cover:

- Why certain narratives dominate sustainable finance

- The gap between market-led thinking and policy reality

- Whether current approaches are set up to deliver real impact

- What needs to change for the transition to actually work"

===

Listen:

(530) Canbury: Six Flags Over Texas and Redomicile Proposals

Canbury: Six Flags Over Texas and Redomicile Proposals

(https://proxypro.substack.com/p/six-flags-over-texas)

Companies are leaving the shareholder-aligned—or at least well-defined—confines of Delaware for the corporate-friendly open plains of Texas. Recent reforms to the Texas Business Organizations Code (TBOC), along with the 2024 launch of the specialized Texas Business Court, have attracted a wave of companies to propose redomiciling in the Lone Star State. The concern among institutional investors is what rights are they losing to hold boards accountable in the Texas shuffle.

ArcBest saw two-thirds shareholder approval for its redomicile proposal in April, while Texas Capital Bancshares narrowly experienced defeat. ExxonMobil has its proposal going to a shareholder vote later this month, along with a number of other companies this season, including Dell Technologies.

Taking a page from Six Flags amusement park - named after the six sovereign flags that have flown over Texas - Canbury Insights’ ProxyPro platform uses a six-flag assessment for scoring companies on their redomicile proposals. The ride can be thrilling or terrifying, depending on where you are sitting.

Please note that this is absolutely, positively not voting advice, nor investment advice, but definitely not voting advice. You read beyond this point at your own risk and with clear understanding that this is not voting advice.

(524) Generation IM: How Physical World AI Could Reshape our Economy

Generation IM: How Physical World AI Could Reshape our Economy

At a glance:

- Over $34 billion of private capital flowed into robotics-related companies in 2025 – more than twice that of 2024.1 Yet some of the best-funded companies are still in the early stages of commercialisation, with scaled deployments years away.

- Physical world foundation models, which include both vision language action and world models, are emerging as the next frontier of artificial intelligence, but data remains a critical bottleneck.

- We see investment opportunities in robotic hardware and the software ‘picks and shovels’ of physical AI, including companies providing data, testing infrastructure and simulation tools.

(515) RIBI™ 2026: The Responsible Invesment Brand Index

RIBI™ 2026: The Responsible Invesment Brand Index

(https://www.ri-brandindex.org/download-ribi-2026/?mc_cid=7ef92bd8bc&mc_eid=170a9b7c5e)

Clarity Turns Conviction into Competitive Edge

"The landscape of responsible investment has entered a new and more demanding phase. One that rewards clarity above all else. The debate has moved on from questioning the meaning of sustainability, to questioning

whether it is practised intentionally and from within. If so, what is the intent? Regulatory pressure, performance disappointments, and political backlash have exposed the difference between asset managers for whom responsible investment is a genuine part of who they are, and those for whom it was always a posture.That difference is now more visible to clients, to regulators, and to the market. Naming it, measuring it, and acting on it is precisely what RIBI 2026 is for."

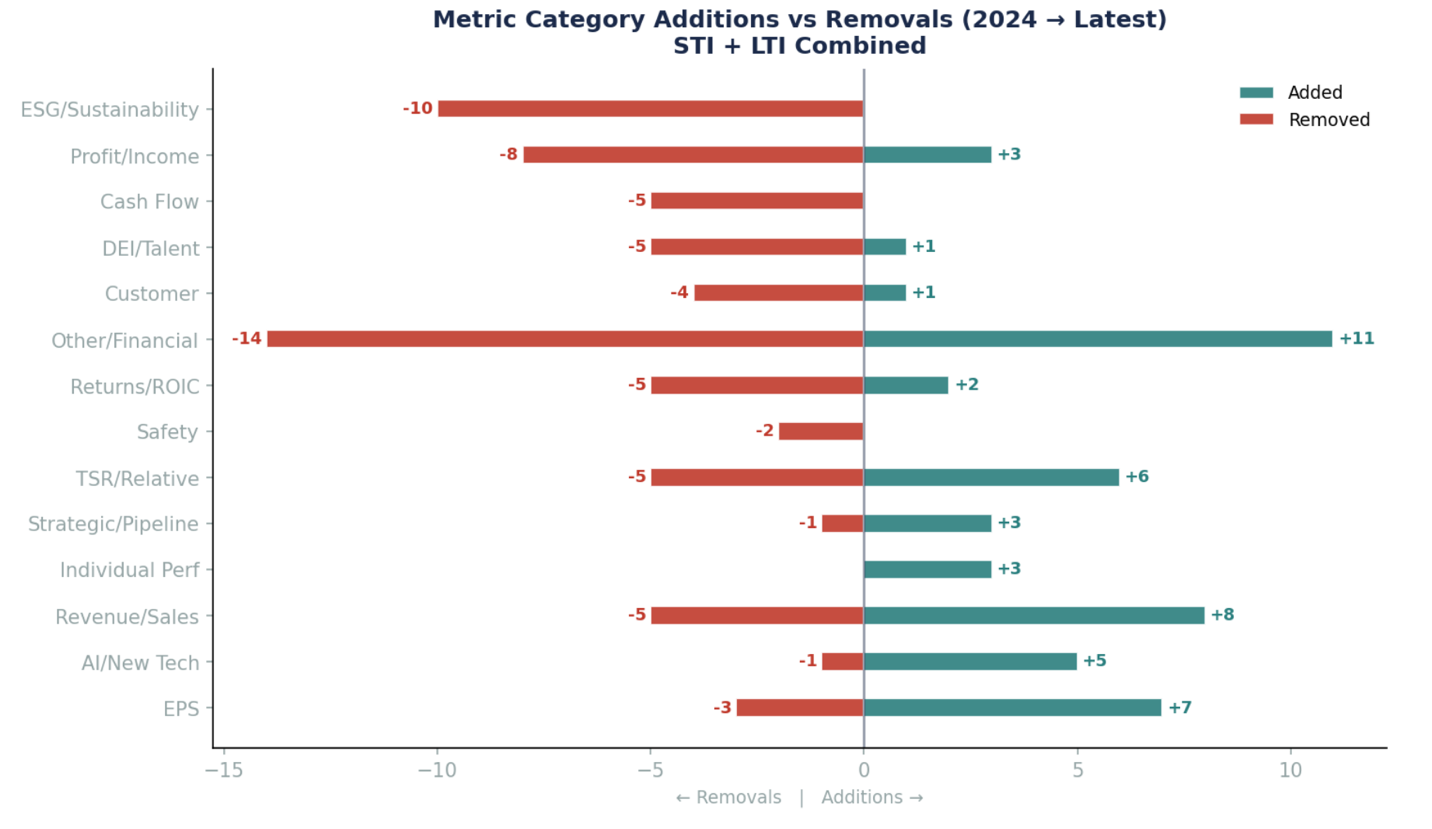

(500) Canbury: ESG Pay Metrics are Out, But What's In?

Canbury: ESG Pay Metrics are Out, But What's In?

(https://proxypro.substack.com/p/esg-pay-metrics-are-out-but-whats)

Airbnb’s proxy out last week saw it strip out all of its “stakeholder” metrics for 2026 to focus on just revenue growth and margins in its short-term executive pay. It is reflective of the trend to simplify pay plans, scrub what seems ESG-related, and focus on financials — especially for companies where share performance has lagged behind. While including sustainability metrics may have signaled a company’s “purpose,” Airbnb execs earning perfect 100% scores on every category in 2025 and near-perfect in 2024 also shows how easy it is to game the goals.

Placing this in context, so far 80 of the S&P 100 have issued a 2026 proxy. From this, certain trends are emerging — and they point in a consistent direction.

(494) JPM: Energy outlook 2026: Mitigating volatility with a diverse energy mix

JPM: Energy outlook 2026: Mitigating volatility with a diverse energy mix

(https://www.jpmorgan.com/insights/global-research/outlook/energy-outlook)

Key takeaways

- Volatile oil prices and surging electricity demand highlight the urgent need for a diversified energy mix to safeguard economic and energy security.

- The need for diversified energy sources is rapidly reshaping global power generation. Renewables and advanced technologies are projected to supply the majority of global electricity by 2100.

- Overall, increased global investment in renewables, including nuclear, solar and wind, is paving the way for a more stable and resilient future.

(494) Wellington: Yes, climate change (still) matters in private markets

Wellington: Yes, climate change (still) matters in private markets

(https://www.wellington.com/en/insights/climate-change-private-equity)

How do climate-related risks and opportunities intersect with corporate strategy?

"We believe the risks and opportunities associated with climate change (both the energy transition and the worsening events exacerbated by climate change) should be evaluated through the lens of financial materiality. The resulting prominence within corporate strategy will naturally differ by industry and business model ..."

... includes ...

- How do climate-related risks and opportunities intersect with corporate strategy?

- What are the climate-related disclosure expectations for private companies?

- How can Wellington’s value creation and climate resources help our private companies?

- Appendix A: Climate questions to expect from public-market investors

Most viewed job posts

(2227) JobPost: DHL Group - Account & Sustainability Manager (Birmingham UK)

JobPost: DHL Group - Account & Sustainability Manager (Birmingham UK)

Please be aware that interviews are provisionally scheduled to take place during the week commencing 18th May 2026. Applications received after this date may not be considered but will be added to our talent pool for future opportunities, subject to your consent.

(2201) JobPost: LGPS Central - Responsible Investment & Stewardship Analyst (Wolverhampton, UK)

JobPost: LGPS Central - Responsible Investment & Stewardship Analyst (Wolverhampton, UK)

(https://recruitment.cezannehr.com/shared/job/responsible-investment-stewardship-ana-88fed/Linkedin)

LGPS Central (LGPSC) Ltd is the FCA regulated asset manager for eight local authority pension funds across the Midlands.

(2102) JobPost: PRI - Associate, Product Owner (Family Leave Cover) - 9 Month FTC

JobPost: PRI - Associate, Product Owner (Family Leave Cover) - 9 Month FTC

(https://app.beapplied.com/apply/dxcrosogrc)

Location Hybrid · London, UK

Team - Ri SolutionsSeniority - Junior

Closing: 11:59pm, 3rd May 2026 BST

(1989) JobPost: BNP Paribas - Senior Sustainability Consultant (London)

JobPost: BNP Paribas - Senior Sustainability Consultant (London)

(https://group.bnpparibas/en/careers/job-offer/senior-sustainability-consultant?src=JB-12380)

We are seeking an experienced Senior Sustainability Consultant to play a key role in growing our ESG consultancy offering. Working closely with our UK and international sustainability specialists you will support business development, strengthen our market presence, and promote our innovative sustainability services. The role is a blend of technical ESG expertise, client relationship and project management, providing crucial support to investors, asset managers, and corporate occupiers as they navigate regulatory demands, investor expectations, and operational performance goals

Most viewed organisations

- (21) Aberdeen Investments

- (6) SRI-CONNECT

Most viewed users

- (21) Mike Tyrrell @ SRI-CONNECT

- (2) EMILY HOMER @ Robeco

The most recent report on SRI-CONNECT's reach and progress (below) demonstrates the increasingly important role that the site plays in growing and developing SRI & corporate governance research globally.

SRI-CONNECT believes in evidence-based decision-making and we hope that the evidence below will convince anyone exposed to SRI & corporate governance research that SRI-CONNECT is the essential place to be active and to be seen.

Please get in touch if you have any questions or comments.